Tech stocks have soared this year. With massive cash flows and some of the most envied AI-powered earnings growth stories out there, it can make sense to look no further than the Magnificent Seven companies for tech exposure. However, with the Federal Reserve open to cutting rates before inflation falls to 2%, perhaps the hyper-growth, high-multiple innovators (like SNOW, MRVL, and HUBS) are poised to pick up the slack from here.

It’d be a mistake not to consider other tech firms that may be setting a foundation for a meteoric rise on the back of AI and other disruptive, emerging technologies. Not every firm can be Nvidia (NVDA), but the following trio of tech stocks may have more to offer than the Magnificent Seven at today’s multiples.

Let’s use TipRanks’ Comparison Tool to compare the three aforementioned tech firms with powerful and perhaps underrated growth drivers.

Despite crashing nearly 48% from its February peak to its June trough, Snowflake still doesn’t look cheap in a traditional sense at more than 243 times forward price-to-earnings (P/E) and 14.7 times price-to-sales (P/S). That said, its new leader, CEO Sridhar Ramaswamy, probably knows more about AI than most other top tech executives.

After all, he founded an AI search firm, Neeva, that Snowflake bought outright. With an AI-first leader, a slew of new AI growth drivers (like managed AI service Cortex), and the confidence of Wall Street analysts, I’m staying bullish on the stock.

Goldman Sachs (GS) analyst Kash Rangan is one of the notable bulls on Snowflake stock. He has a Strong Buy rating on the name with a $220 price target, implying over 60% gains from current levels. Snowflake stock is also on Goldman’s “Americas Conviction List” after its latest spill.

Indeed, Rangan is one of the few analysts who’s a big believer in Snowflake’s new CEO. He views Ramaswamy’s AI background and “product-oriented” approach as an asset for Snowflake as it adds to Snowflake’s “innovation engine.” Notably, Rangan thinks Ramaswamy’s hands-on approach could help Snowflake achieve revenue growth of over 30% over time.

As Snowflake adds new AI-driven products to the mix, it will be even better equipped to take advantage of the AI boom as it spreads to software platforms and infrastructure plays. Though only time will tell when SNOW stock is ready to explode again, Rangan is right on the money when he says Snowflake’s trading at “an attractive entry point.”

SNOW stock is a Strong Buy, according to analysts, with 25 Buys and eight Holds assigned in the past three months. The average SNOW stock price target of $200.97 implies 48.8% upside potential.

Marvell Technologies stock is another AI beneficiary investors have not yet fully appreciated. Shares of the fabless semiconductor firm are up a mere 3.7% in the past year, trailing not only the semiconductor index but also the S&P 500 (SPX).

Earlier this week, JPMorgan (JPM) analysts highlighted Marvell as one of its top chip stock ideas. The firm’s role in custom AI ASICs (application-specific integrated circuits) is a major reason for this. As a less-appreciated chip play that’s still 27% off its all-time highs, I’m inclined to stay bullish on the name.

Another big-name bull on Wall Street, Goldman Sachs’ (GS) Sung Cho, sees Marvell doubling sales from current levels. Aside from the demand for custom AI ASIC chips, Cho sees Marvell as a beneficiary of data center growth. With a strong slate of networking equipment (think adapters and switches), Marvell stands out as a picks and shovels play for the rise of the data center.

At 48.5 times forward P/E, MRVL stock is trading at the low end of its past-year historical range. Given the magnitude of catalysts ahead, Wall Street seems right to be pounding the table right now. Marvell may be the semiconductor stock that got left behind, but probably not for long, as its multiple growth drivers begin gaining traction.

Sure, it’s a diversified semiconductor play that will benefit from future phases of the AI revolution. Nonetheless, patient investors looking for a catch-up play in semiconductors may have the perfect one with MRVL stock at around $68.

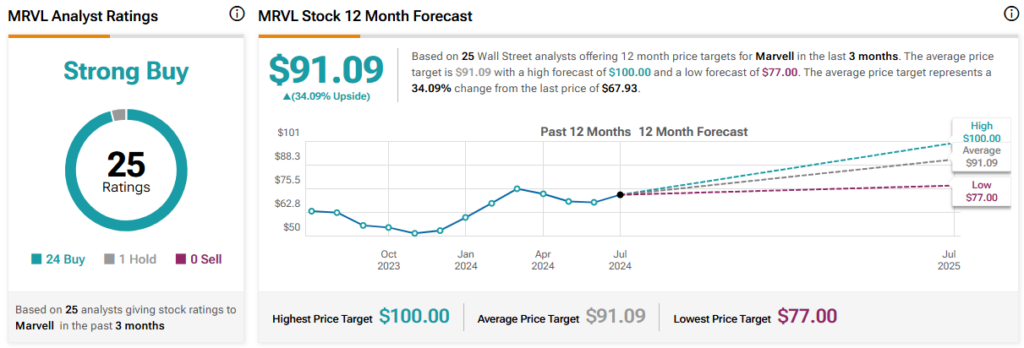

MRVL stock is a Strong Buy, according to analysts, with 24 Buys and one Hold assigned in the past three months. The average MRVL stock price target of $91.09 implies 34.1% upside potential.

AI-driven CRM (customer relationship management) software developer Hubspot may have recently lost a suiter in Alphabet (GOOGL). However, the recent 11% correction that ensued seems more like an opportunity to buy, even as takeover speculators begin rushing to the exits. Despite Google being out of the running, other interested acquirers may have a chance to buy up the firm down the road (Amazon (AMZN) is reportedly interested).

Deal or not, I’m staying bullish on HUBS stock, as it’s a very fast-rising SaaS (Software-as-a-Service) company that’s becoming difficult to ignore.

At writing, shares of HUBS go for 66.6 times forward P/E, which is on the low end of the past-year range (shares went for over 110 times next year’s expected P/E earlier last year).

For a firm that can sustain double-digit growth and meaningful operating margin expansion, the seemingly hefty premium seems more than worth paying. For Q1 2024, Hubspot clocked in 23% in sales growth year-over-year. Additionally, operating margins have slowly but steadily crept higher in recent years.

Back in March, Hedgeye praised HUBS stock as one of its long ideas, noting it’s a “standout” SaaS competitor capable of growing over the long haul. Since the note, the stock has only gotten cheaper. Maybe it’s time to back up the truck now that the Google deal has backed away.

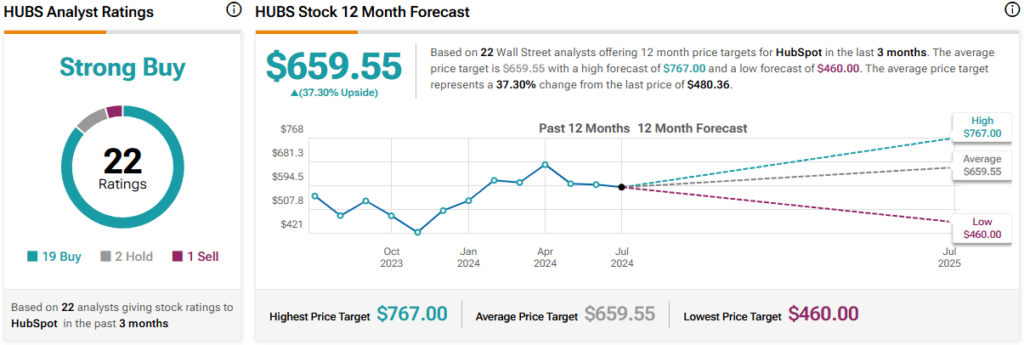

HUBS stock is a Strong Buy, according to analysts, with 19 Buys and two Holds assigned in the past three months. The average HUBS stock price target of $659.55 implies 37.3% upside potential.

The following Strong-Buy-rated technology stocks may not be making new highs, but they’re still “growthy” companies that lack the same degree of hype as some of the other high-tech AI names that have gone parabolic lately.

Of the three names, analysts see SNOW stock as having the most room to run (48.8%) from current levels. I agree with analysts that Snowflake is the strongest buy right here. Snowflake CEO Sridhar Ramaswamy has given the data cloud company an AI shot in the arm. For now, though, the market has its doubts about the firm’s ability to get back on the growth track.

and their net worth | NFL News – The Times of India")