The technology sector has been the primary driver of market gains since early last year, with the boom in AI stocks setting the tone. The tech-heavy NASDAQ index is now within 3% of the all-time high it reached earlier this month.

All of this raises the question: is now the time to buy into tech stocks? Youssef Squali, a 5-star analyst rated in the top 4% of the Street’s stock pros, argues that it is. He recommends that investors pick up shares in the tech mega-caps Alphabet (NASDAQ:GOOGL) and Meta Platforms (NASDAQ:META) ahead of their upcoming earnings releases.

Let’s take a closer look at these tech titans and Squali’s comments to understand why he considers them compelling choices.

Alphabet

We’ll start with Alphabet, the parent company of both Google and YouTube, which places it in a leading position in online search and digital advertising. Controlling these two leading search engines and their associated ad services has been highly lucrative for Alphabet; the company credits ‘Google advertising’ with approximately three-fourths of its total revenue. Investors have generally been impressed with Alphabet in recent years, and their interest has translated into a market cap of $2.25 trillion, making the company the fourth-largest publicly traded firm on Wall Street.

If you’re looking for a mega-cap tech with a solid foundation, it’s hard to find a better one than that. And Alphabet has been making proactive moves to maintain its position as a tech industry leader. The company has multiple AI projects in play, with the most prominent being Gemini. More than just an AI-powered search tool, Gemini includes generative AI tech as well as multimodal large language models in its make-up, and promises to bring strong improvements to the full range of Google functions. These include internet search, of course, but also include online translation services and generative AI text creation. The company aims to give Google a competitive edge against Microsoft’s Bing, a chief competitor that has already integrated generative AI into the search results, as well as giving Google the ability to compete against gen-AI content creation tools such as ChatGPT.

The company’s profits have been on an upward trend in recent quarters, with the 1Q24 report showing a top line of $80.54 billion. That was up 15% from 1Q23 and beat the forecast by $1.84 billion. It supported Alphabet’s bottom line, an EPS of $1.89. The EPS figure beat the forecast by 39 cents per share, and was up more than 61% year-over-year.

Alphabet is set to release its 2Q24 earnings today after market close. The company is expected to show revenues of approximately $84.3 billion and a bottom line of $1.84 per share. Achieving those figures will represent a y/y revenue gain of 13%, and a y/y EPS gain of 27%.

Top analyst Youssef Squali is bullish on Alphabet, citing the company’s continued success in engaging users and its momentum in the cloud computing and digital advertising sectors.

“We remain positive on GOOGL ahead of 2Q24 results as we believe the quarter will show in line or slightly better top line growth fueled by healthy user engagement across Search and YouTube (with higher CPMs) and sustained performance in Cloud. We expect Opex containment to protect margins even as Capex rises. Conversations with digital ad agencies suggest that the momentum seen in 1Q was sustained in 2Q across Search and YouTube, with strong results from Travel, CPG, and Retail,” Squali opined.

These comments back up the analyst’s Buy rating on Alphabet stock, although his price target of $190 points toward a relatively modest one-year gain of 4% for the shares. It will be interesting to see if the analyst revises his target following the earnings release. (To watch Squali’s track record, click here)

Overall, GOOGL boasts a Strong Buy consensus rating based on 39 recent analyst recommendations, which include 33 Buys to 6 Holds. The stock is trading for $182.39 now, and its $202.88 average target price is somewhat more bullish than Truist allows, suggesting an 11% gain on the one-year horizon. (See GOOGL stock forecast)

Meta Platforms

Founded originally as Facebook, Meta Platforms, the brainchild of Mark Zuckerberg, quickly became enormously profitable and expanded by acquiring competing social media platforms. Today, Meta is a leader in social media, serving as the parent company of Facebook, Instagram, Messenger, and WhatsApp. Through these apps, Meta reaches a global audience, transcending language and geographic barriers, and boasts a user base exceeding 3 billion people.

Meta’s core business model revolves around monetizing its social media platforms through digital advertising. That, in turn, rests on the success of the company’s reach – and with its 3-plus billion user base, Meta has plenty of leverage in that field.

Furthermore, Meta has positioned itself as a notable AI developer. The company integrates AI into its metaverse social media model and its digital advertising business. Meta’s AI research lab is pursuing various avenues, including creative and generative AI, as well as connection AI. These technologies enhance user experiences by tailoring suggestions – ads, posts, potential connections – based on individual user activity. Meta envisions a seamless transition between the real world and the AI universe, aiming to make AI scalable to each user’s comfort level.

Getting to the bottom line, this is big business. Meta is another of Wall Street’s trillion-dollar-plus companies, with a market cap of $1.2 trillion putting it in sixth place among the largest firms traded on Wall Street.

Meta reported strong financial results in Q1 of this year and is expected to continue this trend in Q2, with results due on July 31. For Q1 2024, Meta’s revenue reached $36.46 billion, marking an impressive 27% year-over-year gain and surpassing expectations by $240 million. The company’s earnings were $4.71 per share in the first quarter, 39 cents above the anticipated figures.

Looking ahead, analysts expect to see revenues of $38.28 billion in Q2, a total that would indicate a nearly 20% y/y gain. The bottom line for Q2 is expected to come in at approximately $4.74 per share. Meta’s management itself has published Q2 revenue guidance giving a range of $36.5 billion to $39 billion.

Truist analyst Squali expects Meta to hit those targets, noting: “We remain constructive on META into 2Q24 earnings as we expect the quarter to come in at the high-end of mgmt’s guidance for revenue growth, fueled by sustained global ad demand and higher CPMs. We believe Meta’s significant AI investments are yielding better ranking & recommendation results for users and advertisers, driving better outcomes for both and fueling above-industry revenue growth.”

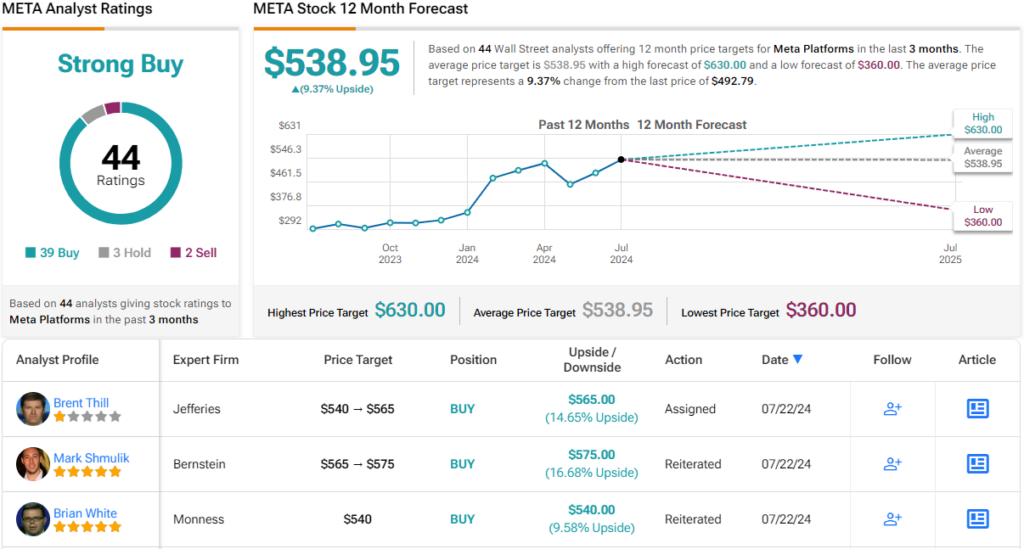

To this end, Squali rates Meta stock as a Buy, and his $535 price target indicates potential for a one-year gain of 9%.

The Street’s outlook is generally in line with the Truist view. The stock has a trading price of $493.11 and its $538.95 average target price suggests a 9% one-year increase from that level. The shares have 44 recent analyst reviews, breaking down to 39 Buys, 3 Holds, and 2 Sells, for a Strong Buy consensus rating. (See META stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.

and their net worth | NFL News – The Times of India")