")

fizkes

In this market, Zoom Video (NASDAQ:ZM) is an intriguing pick. The tech company has some of the slowest growth rates among tech peers, but its high profit margins and low stock valuation make it highly compelling. Net cash makes up 40% of the market cap, and the company is repurchasing stock. Wall Street may be underestimating the possibility that growth returns as post-pandemic headwinds may eventually subside. Yet, the stock looks quite attractive even assuming anemic top-line growth. I am upgrading the stock to strong buy.

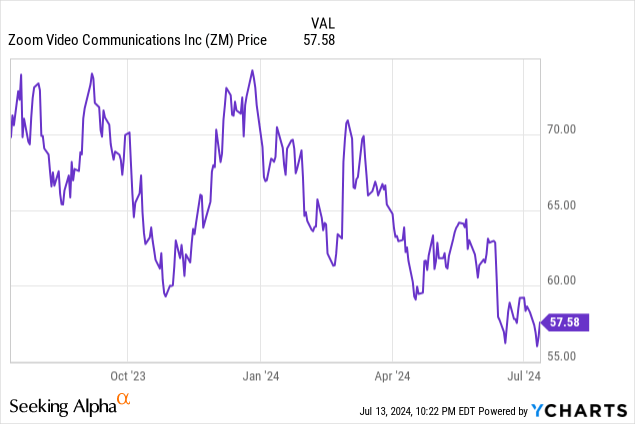

I last covered ZM in April, where I stood by my bullish view on the stock due to the large net cash position and share buyback program. The stock has been underperformed the broader market since then, which makes sense given the lack of excitement in recent quarters.

Do not let the lack of upward volatility fool you – I view ZM to be a coiled spring, as investors may inevitably come to appreciate the deep value in the stock.

ZM is best known as being a consumer and enterprise tech company powering video conferences, but it also offers products spanning all workplace communication.

FY25 Q1 Presentation

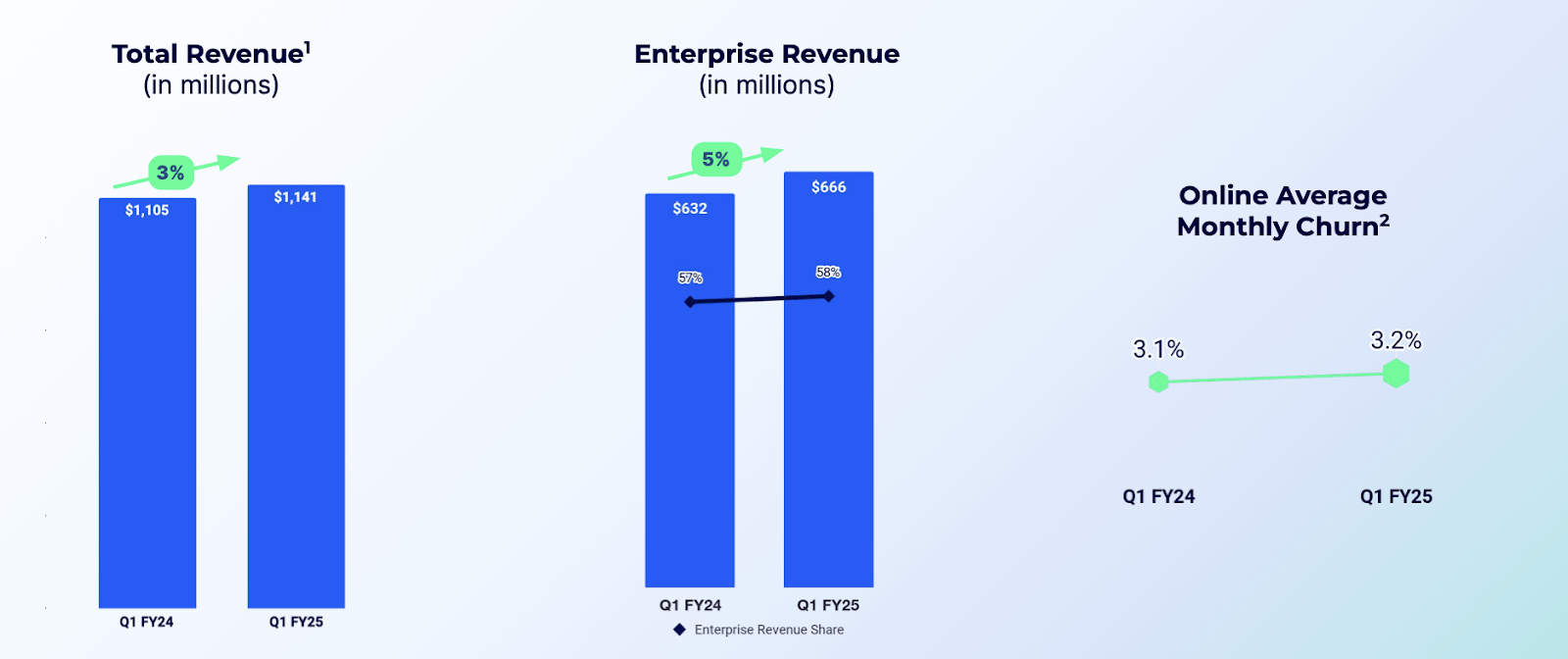

In its most recent quarter, revenues grew 3% YoY to $1.141 billion, slightly surpassing guidance for $1.125 billion. I am doubtful that many investors were enthused by the guidance beat, given the low growth rate.

FY25 Q1 Presentation

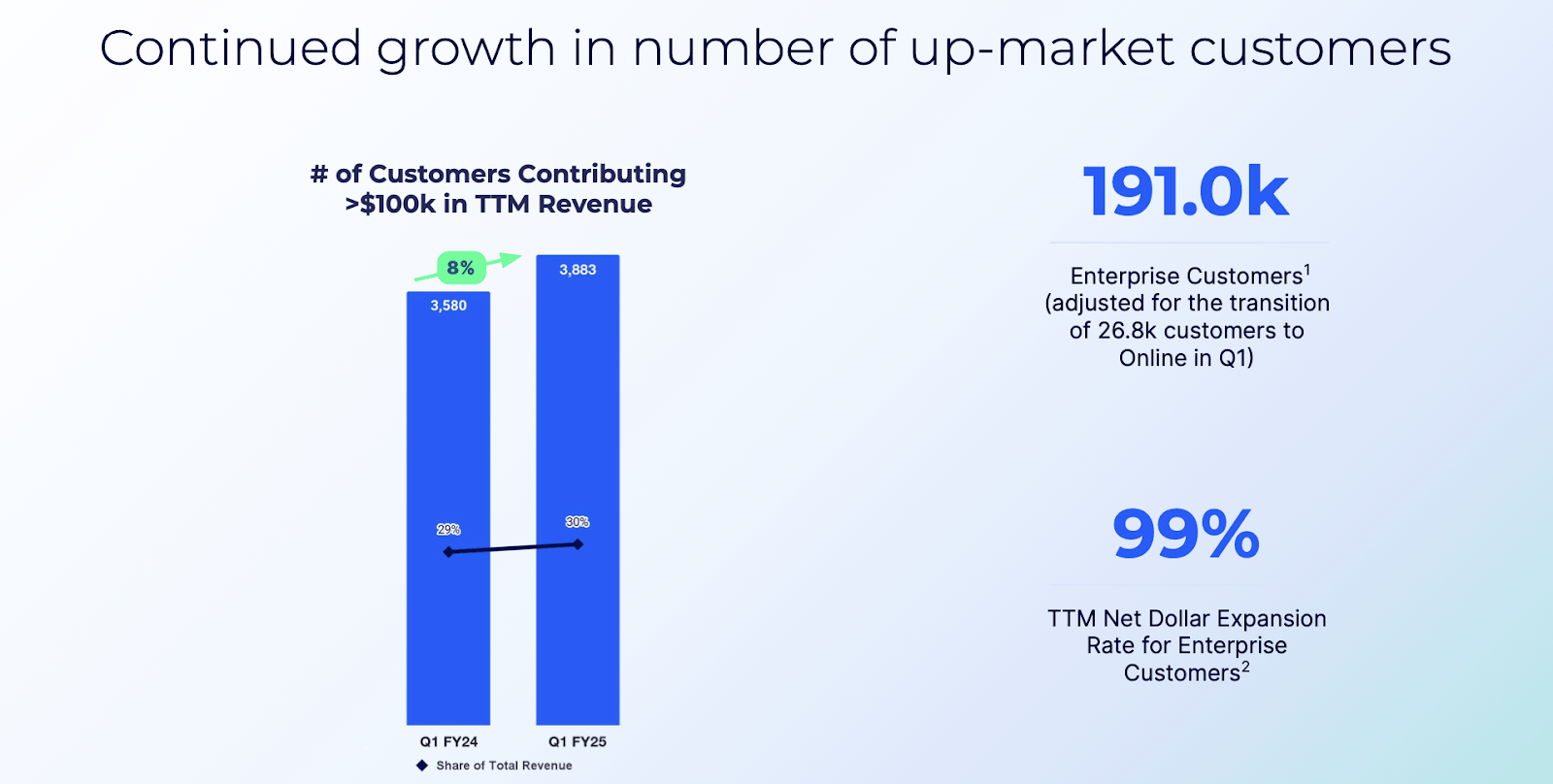

I suspect most investors focus on the enterprise business, given the lower level of cyclicality. Unfortunately, the net dollar expansion rate continued to decelerate, coming in at 99%. That said, this is not too surprising given that companies all around have been tightening IT budgets and limiting headcount growth amidst the higher interest rate environment. On top of that, ZM is likely still suffering from post-pandemic headwinds, as it had seen a dramatic pull-forward in growth during the pandemic. At some point, I expect both these headwinds to subside, leading to solid single-digit top-line growth.

FY25 Q1 Presentation

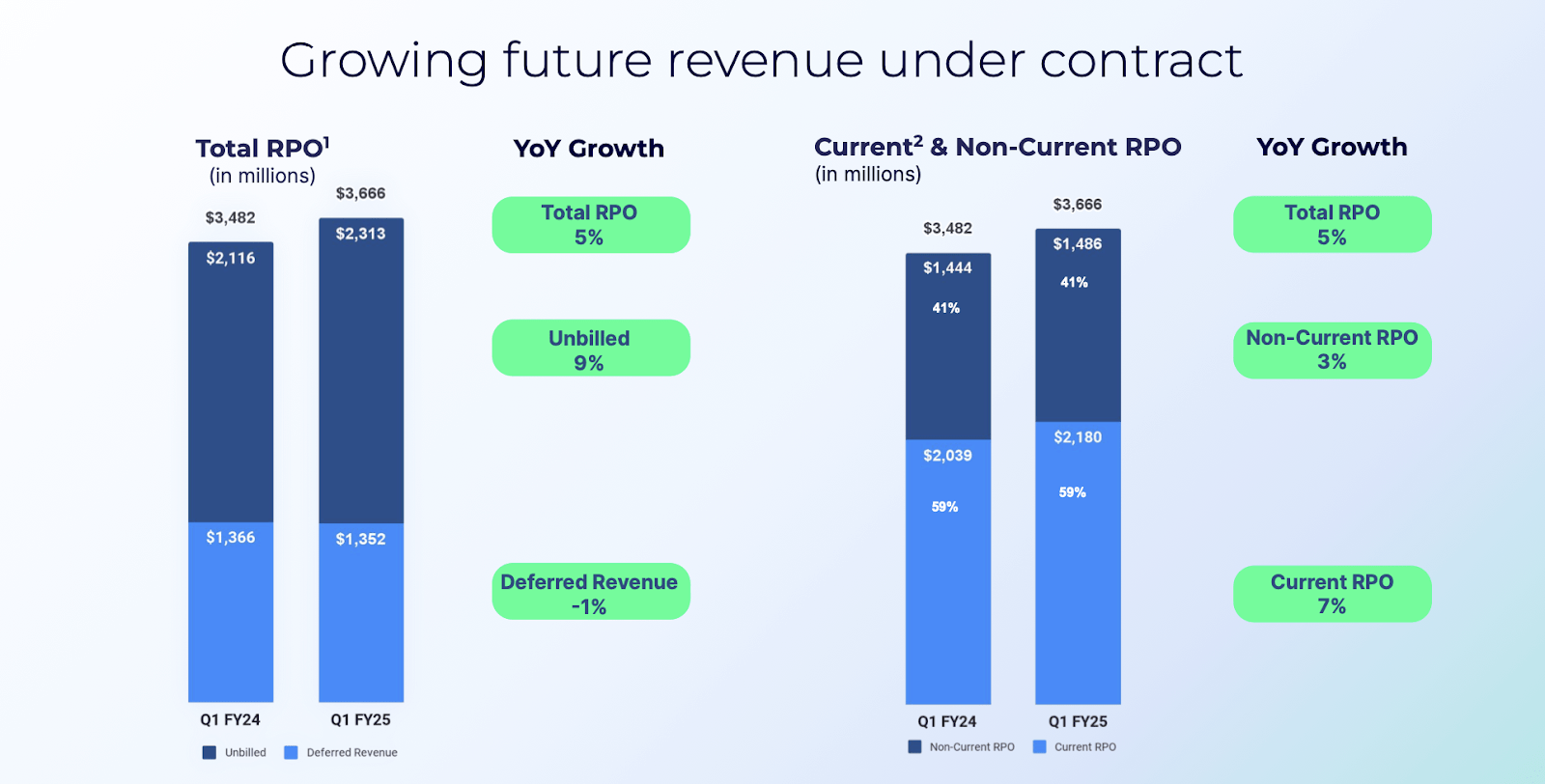

ZM posted solid growth in remaining performance obligations, especially with current RPO growing 7% YoY. I view cRPO growth as being a potential indicator of future revenue growth, though it should be noted that revenue growth has trailed cRPO growth for several years.

FY25 Q1 Presentation

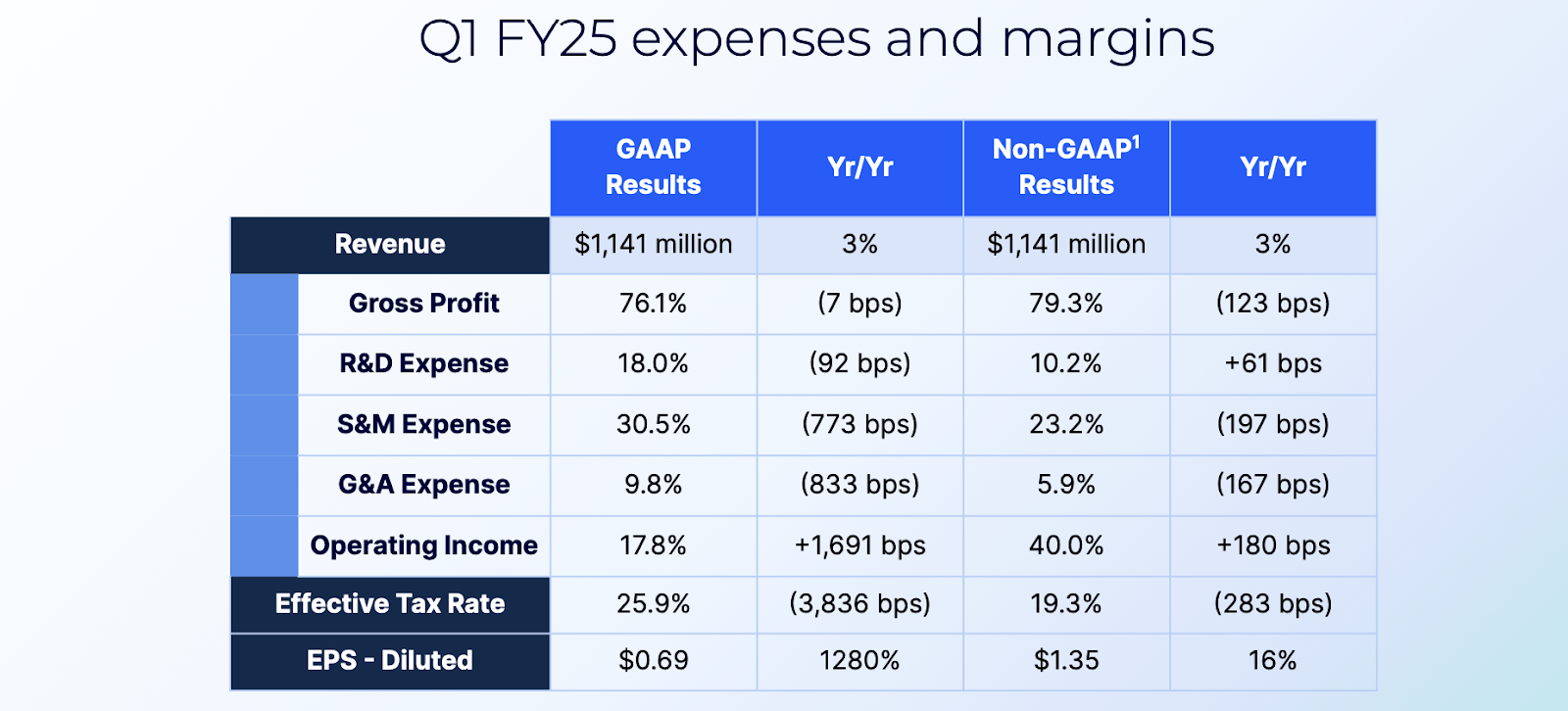

On the profitability front, ZM delivered solid margin expansion on both GAAP and non-GAAP fronts, delivering $1.35 in non-GAAP EPS (exceeding guidance of $1.18 to $1.20).

FY25 Q1 Presentation

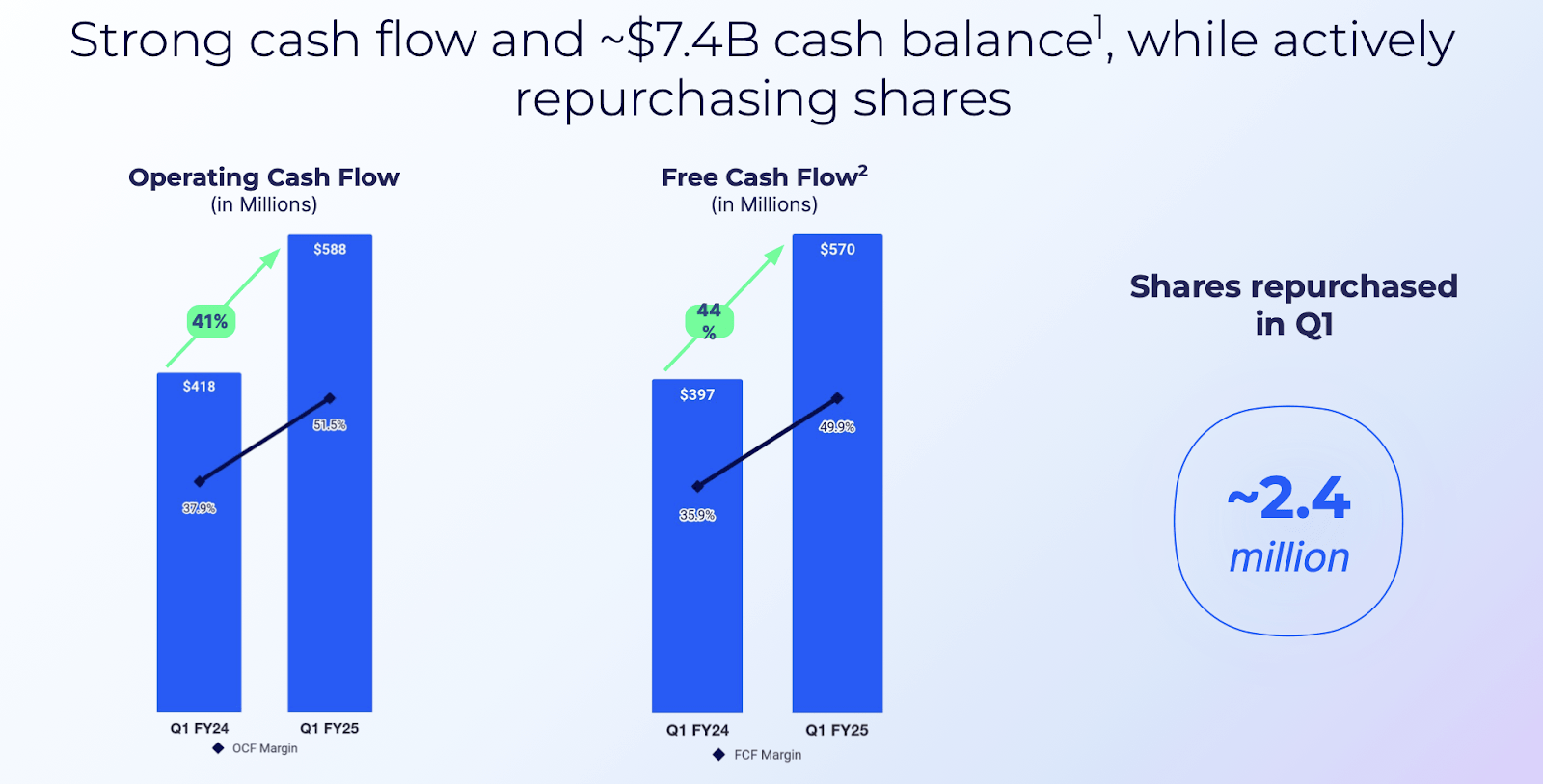

Free cash flow exceeded non-GAAP profits, with the company generating $570 million of FCF in the quarter. ZM ended the quarter with $7.4 billion in cash versus no debt, representing around 40% of the market cap. The company repurchased 2.4 million shares for $150 million in the quarter. That’s a bit lower than I was hoping for, but is a good start.

FY25 Q1 Presentation

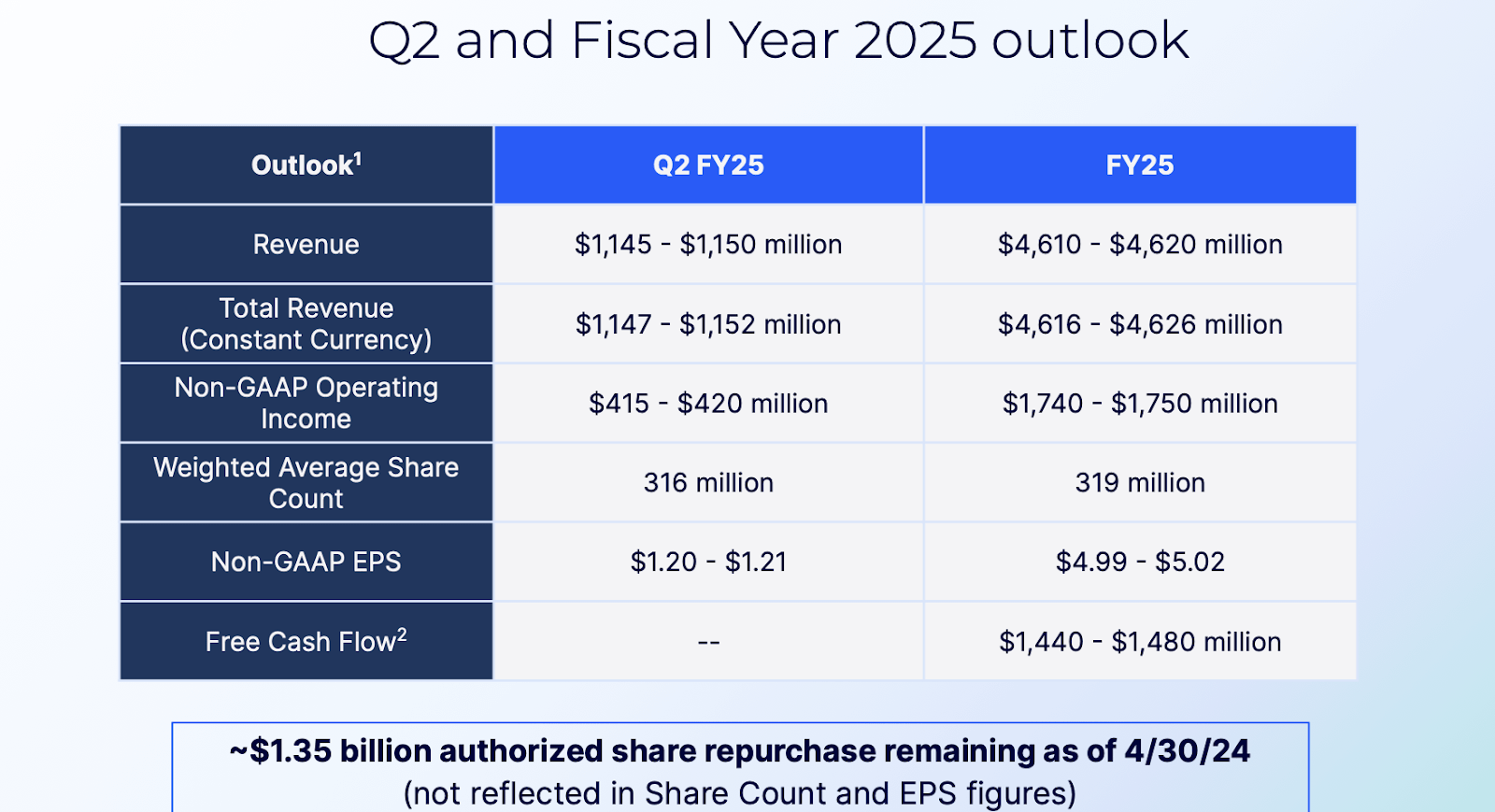

Looking ahead, management has guided for the second quarter to see just 1% YoY revenue growth to $1.15 billion at the high end (consensus estimates expect the same). Management slightly raised full-year guidance from $4.6 billion to up to $4.62 billion in revenues. Management also now expects up to $5.02 in non-GAAP EPS.

FY25 Q1 Presentation

On the conference call, management noted that the slight uptick in online churn to 3.2% was due to a “tightening up of the grace period for unmade payments,” and estimated that it would have remained consistent at 3% without those changes. Management noted that they transitioned 26,800 Enterprise customers to the Online bucket in order to “improve the customer experience and drive greater efficiency” in their operations. These customers accounted for just $4 million of aggregate revenue, and this change did not impact the aforementioned 99% net dollar expansion rate. Management expects the second quarter to be a proverbial bottom of the business, with growth accelerating thereafter. This makes some sense, if only given that the company had seen YoY growth peak at 5% constant currency in the first quarter last year before decelerating thereafter, suggesting that the company will begin lapping easier comparables.

Management noted that Zoom Contact Center was gaining traction, reporting 90 customers with over $100,000 in ARR, representing growth of 246% YoY. That said, this product is still very small relative to the more important video conferencing solutions, and I do not expect it to materially contribute to growth for quite some time.

Management mentioned that they are still able to maintain a premium price point for their product, due to customers still wanting “the best video service.” I hope to see more discussions like this given that I expect a multiple re-rating to be a big driver of shareholder returns over the long term, with management needing to convince Wall Street of the recurring nature of the business.

While ZM stock certainly isn’t behaving like it, it is notable that it technically is deserving of being considered an “AI play.” The company has rolled out AI capabilities, including the ability to record summaries of video meetings.

Zoom

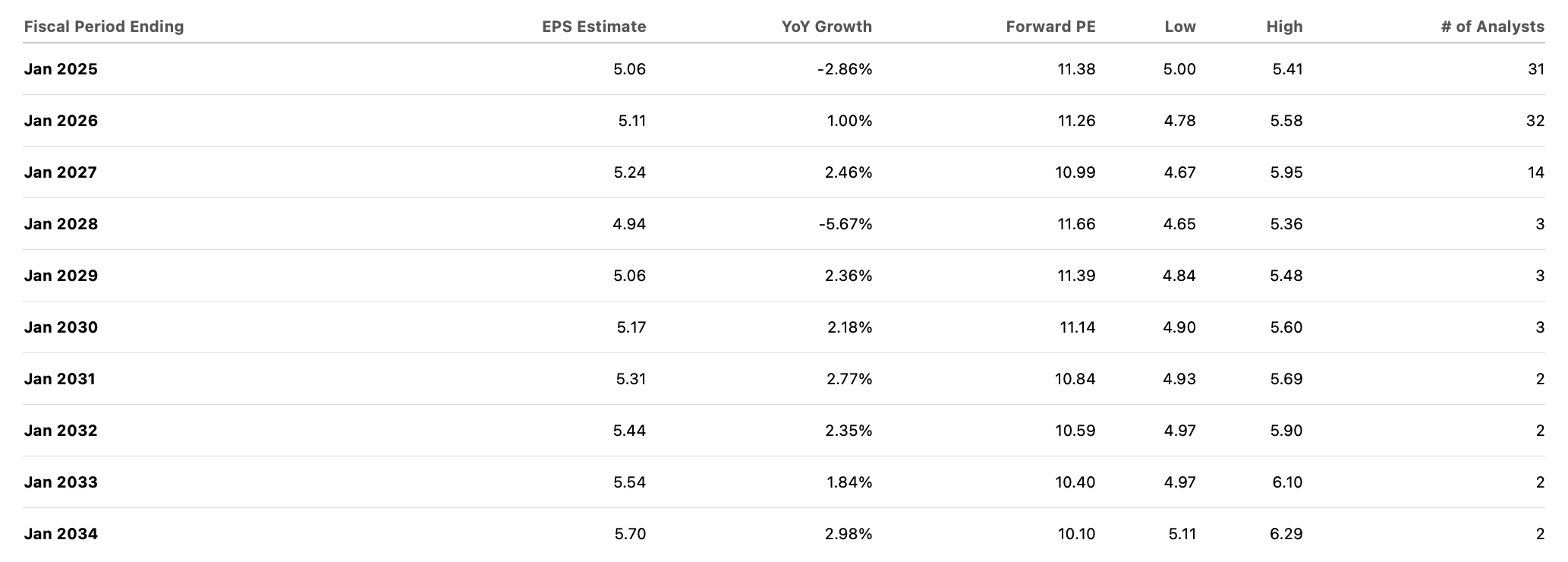

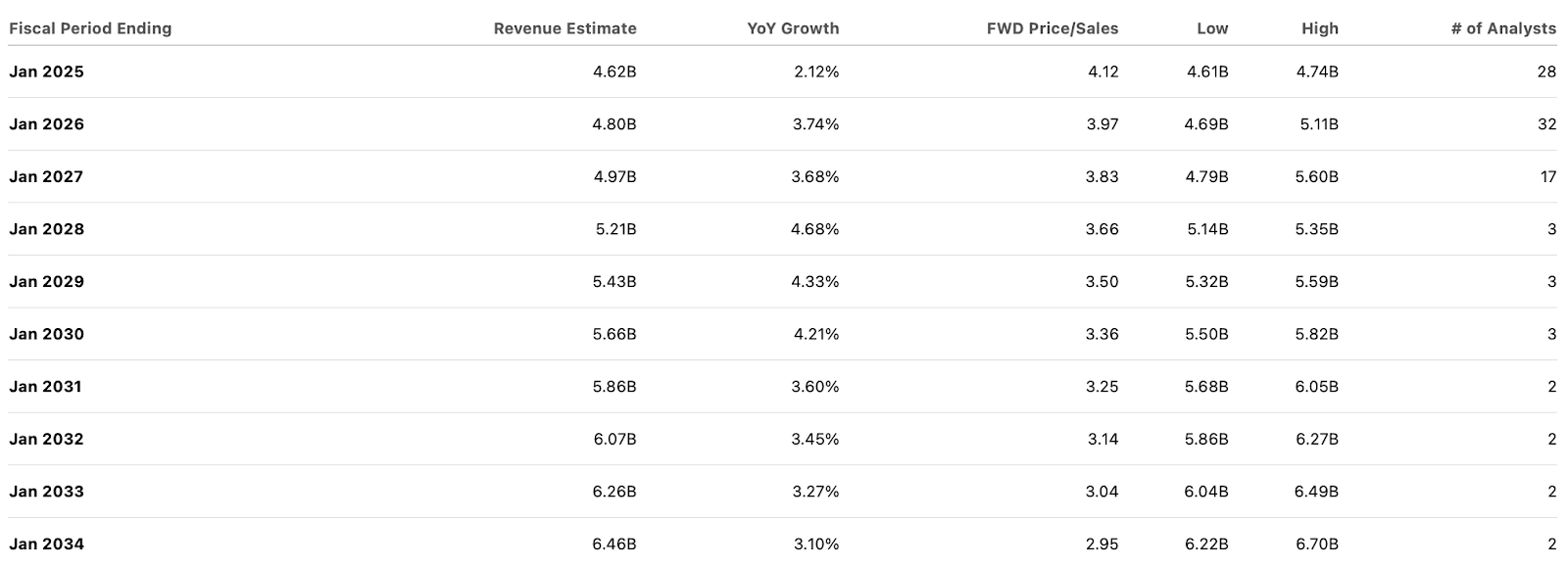

Wall Street has lacked enthusiasm for ZM stock ever since the pandemic peak. This is evident in the stock’s low valuation, trading at just 11.4x this year’s earnings estimates.

Seeking Alpha

It is curious to note that Wall Street consensus estimates still expect the company to generate solid single-digit top-line growth moving forward. Consensus estimates are calling for net margins to deteriorate moving forward.

Seeking Alpha

While it is hard to disagree with the conservative top-line outlook, I find that profitability piece to be too pessimistic. This is a company that generated a 33% GAAP net margin during the pandemic, and gross margins remain high at around 80%. I expect the company to achieve 35% net margins over the long term, if not much higher. I see 20x earnings as an appropriate multiple for a business with net cash, highly recurring revenues, and a low single-digit top-line growth rate. That would place my fair value target at around 7x sales, implying strong multiple expansion potential. There is not any imminently visible catalyst towards driving that re-rating, as it is unclear what it will take to get Wall Street to appreciate the recurring rent-like nature of the revenue base. But perhaps if ZM can start showing operating leverage again, then that may help drive this anticipated re-rating as well as increase the earnings component in the annual return potential. I note that any move to put the 40% net cash position towards accelerated share repurchases might prove to be an important catalyst as well.

I view ZM as having a technologically superior product to Microsoft (MSFT) Teams, but that point might not matter, as customers may find MSFT’s product to be at least “good enough” as there is the convenience of consolidating multiple IT products with one vendor. It is also possible that generative AI or simply time enables MSFT to close the gap on the technological difference, which might increases the churn rate even among enterprise customers. It is possible that ZM sees margins contract due to competition. It is possible that top-line growth rates eventually turn negative if the video conferencing growth story falters or if competition heats up.

ZM is representative of the kind of name I am looking for nowadays: some secular top-line growth, net cash on the balance sheet, and (ideally) very low valuation. The company’s low revenue growth rate may hold back the stock in the near term, but eventually, I see the stock re-rating as Wall Street comes to appreciate a recurring, cash flowing business. I like the margin of safety between the low valuation, high cash flow generation, and 40% net cash position. I am upgrading the stock to strong buy.

and their net worth | NFL News – The Times of India")