Americans love sports, that’s for sure – and they love sports betting, too. It’s not so much the gambling that’s attractive. Rather, it’s the chance to get some more skin in the game, to have as much riding on the game as the players. At the regulatory level, more and more states are legalizing it as entertainment, either online, in casinos, or both. As of this past February, 38 states permit some form of the practice, and of those, 29 permit online betting.

As far as stocks go, the odds here are all in favor of the investor. Sports betting rakes in oodles of cash; globally, the sports betting market was worth $81.7 billion in 2022, and by 2032 is expected to reach as high as $231.2 billion. The predicted decadal increase, if achieved, will represent a CAGR of 11.1%.

Covering the sports betting world for Goldman Sachs, analyst Benjamin Miller has taken the measure of the industry’s potential, writing, “We believe there is an opportunity to marry sports & gambling content to drive more engagement and favorable bet type mix (i.e. more in-play betting) as the fan experience shifts from passive viewership to being more interactive as media brands look to integrate technology alongside the streaming rights they’ve acquired… We’ve already seen a number of examples of how the media industry has evolved and incorporates gambling content as legalized gambling becomes widely accepted and regulated.”

Miller has gone on to look at two big names here, DraftKings (NASDAQ:DKNG) and Genius Sports (NYSE:GENI), singling them out as prime contenders in the sports betting stocks arena. Let’s take a closer look at both, and at the analyst’s comments.

DraftKings

The first stock we’ll look at, DraftKings, was founded in 2012 and entered the public trading markets through a SPAC transaction in 2020. The company has become one of the US betting market’s fastest-growing sportsbook and fantasy league platforms, providing full packages of betting options and fantasy play to sports fans of all stripes. DraftKings currently operates legal sports betting activities in 26 states.

DraftKings offers fans coverage of a wide range of domestic and international professional sports leagues, including American football, Major League baseball, the NBA, the NHL, and international soccer. College hoops are also hugely popular, although not a pro league, and are also covered in DraftKings’ sports betting platform. On the fantasy league side, DraftKings lets fans build up their ‘dream teams’ of great players – and bet on those teams’ collective performances. Fantasy leagues differ from traditional sports betting by allowing gamers to make pre-game choices that will determine the outcome of the bets.

DraftKings is definitely seeing its own share in the sports betting cash bonanza. The company’s revenues have been on an upward trend for several years now, and that can be seen clearly looking at recent annual totals: a top line of $2.24 billion in 2022, that rose to $3.66 billion in 2023. Meanwhile, DraftKings stock has gained nearly 90% over the last 12 months.

DraftKings isn’t resting on its laurels. This past February, the company announced it had entered into an acquisition agreement with the online lottery firm Jackpocket. Under the terms of the agreement, DraftKings will acquire Jackpocket for a total of $750 million, in a 55-45 split of cash and stock. DraftKings expects to close the acquisition during 2H24, and realize an additional $60 million to $100 million in adjusted net earnings annually by 2026.

DraftKings last reported financial results for 4Q23, and in that quarter showed a top line of $1.23 billion, skating just $10 million below the forecast but growing 44% from the prior year quarter. In earnings, DraftKings realized a non-GAAP EPS of 29 cents, 11 cents per share ahead of the estimates. In an important metric, especially considering the large payments DraftKings will need to make as part of the Jackpocket deal, the company finished 2023 with $1.27 billion in liquid assets. We’ll see on May 2 how DraftKings 1Q24 results turned out.

In his coverage of this stock for Goldman Sachs, analyst Benjamin Miller sees reason for investors to pick up DKNG shares, explaining: “Our Buy rating reflects our framing of a more attractive 12m risk/reward as: 1) We expect DraftKings to compound revenue at 20%+ as it continues to benefit from healthy growth in existing states, as well as future state legalizations across OSB & iGaming; 2) Unit economics, including contribution margin and LTV/CAC dynamics, continue to improve at an increasingly better pace; 3) We see 2-3% upside to Street Revenue in 2024/2025 & 3-4% upside to Street Adj. EBITDA & 4) While the stock is up ~65% over the past 9 months, DKNG is trading at a growth adjusted revenue multiple of 0.15x (vs. its historical average of 0.19x and peers currently trading at 0.17x), which is down ~20% over the same time period.”

Complementing the Buy rating, Miller gives DKNG a price target of $60, pointing toward ~48% upside potential for the next 12 months. (To watch Miller’s track record, click here)

Overall, the consensus from Wall Street is a Strong Buy for DKNG, based on 28 recent recommendations, comprising 26 Buys and 2 Holds. The shares are selling for $40.55, and their $52.23 average target price suggests a one-year gain of ~29%. (See DKNG stock forecast)

Genius Sports

Next up is Genius Sports, a company that combines tech and sportsbooks. Genius Sports is primarily a tech firm, but since its founding in 2016, its aim has been to monetize the ability to ‘reach and activate’ sports audiences. Genius Sports reaches those audiences through iGaming tech services, creating immersive viewing experiences, marketing services, and data-driven content for some of the most widely known names and brands from both the sports and betting worlds. These names include such heavy hitters as Major League Baseball, the Denver Broncos, ESPN, Caesars, 888, and the NFL. Genius has active partnerships with more than 650 sports organizations and generates its databases from the coverage of more than 285,000 sporting events.

At its heart, Genius Sports is a software and data management company, using machine learning and AI to build digital connections throughout the sports ecosystems, including all levels from the teams on the fields to the legal rights holders to the fans cheering in living rooms, pubs, and casinos. Genius Sports has the ability to manage all of this – a data tech firm with a global reach that supports its business partners and their betting customers.

Genius Sports is finding its own support from rising demand. The expansion of legalized sports betting has put a premium on data services, which Genius Sports delivers. The results can be seen in the company’s financial releases. Revenues in 4Q23 were up more than 20% year-over-year to $127.2 million. The company’s Betting Technology, Content & Services segment led the revenue gains, growing 32% from the prior year, with revenue reaching $86.7 million. On earnings, Genius Sports registered a net loss for the quarter, of 17 cents per share. While this figure was 10 cents below the forecast, it was also up from the 59-cent EPS loss reported one year previously. The company does not expect to run losses indefinitely; management has predicted that Genius Sports will be free-cash-flow-positive by the end of this year.

Analyst Benjamin Miller, in his comments on GENI for Goldman Sachs, explains clearly why he believes the company is set up for continued success: “We are constructive on GENI’s competitive position in the broader sports ecosystem and believe that the company will continue to increase its relevance and deepen its integration with clients and partners over time. In addition to the company’s core official data solutions we believe that product innovation will be key to maintaining relevance in a rapidly evolving landscape and point to the ramp of Second Spectrum (computer vision solutions for sports) BetVision (interactive video streaming in sportsbooks) and Edge (automatic pricing tool for sportsbooks) as examples of how GENI’s technology-led approach can support greater monetization from here.”

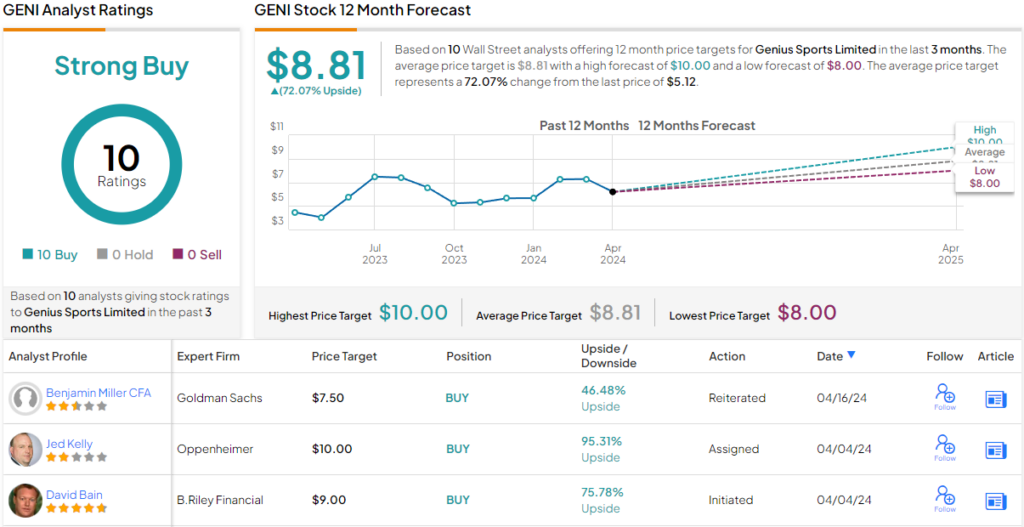

Miller’s constructive view of GENI is summed up in his Buy rating on the stock, and his price target of $7.50 implies the shares will rise by ~46% over the one-year horizon.

The broader view is even more bullish; GENI gets a Strong Buy consensus rating based on 10 unanimously positive analyst reviews. The stock’s average price target of $8.81 suggests a 72% one-year gain from the current share price of $5.12. (See GENI stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.

and their net worth | NFL News – The Times of India")